The 2025 global automotive sales rankings, compiled from OEM-reported figures covering light and heavy vehicles, reveal a market undergoing serious structural change. The rankings are in, and the automotive industry has a new story to tell. Nissan is gone from the top ten. Suzuki has taken its seat. And a Chinese EV giant is quietly rewriting what it means to compete at the highest level. Yes, the names at the very top look familiar.

But look closer, at who fell out, who climbed in, and which Chinese manufacturers are now breathing down the necks of legacy giants, and a much more disruptive picture emerges.

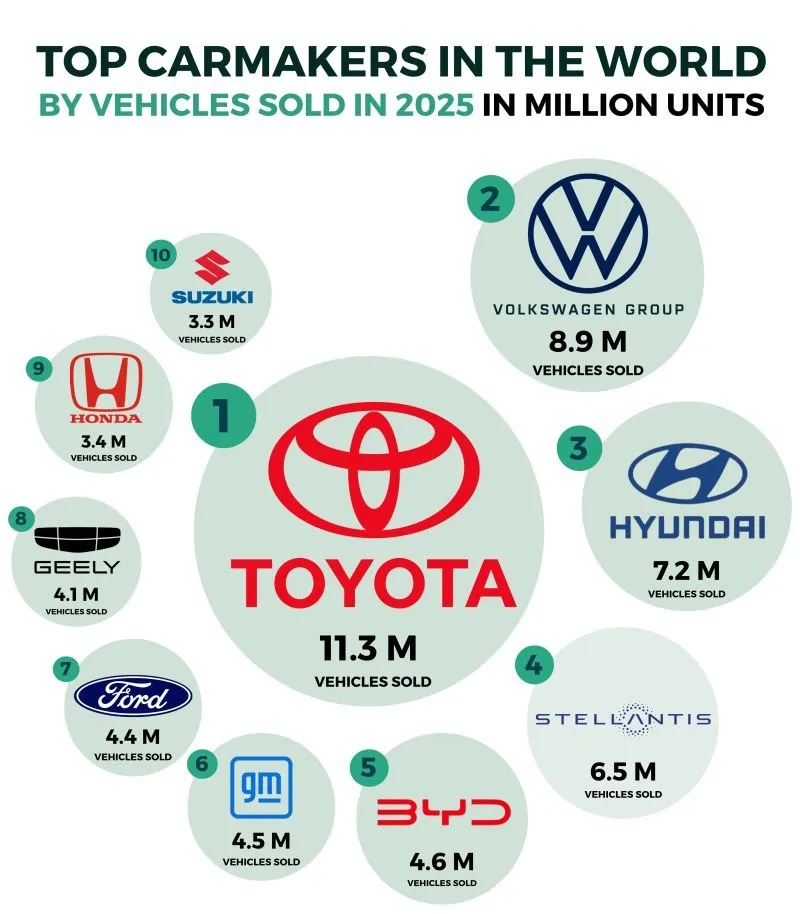

Here is the list of Global Car Sales in 2025.

Rank | Group | Key Brands | Units Sold (2025) |

1 | Toyota | Toyota, Lexus, Daihatsu, Hino | 11,322,575 |

2 | Volkswagen | VW, Audi, Skoda, Porsche, Bentley, Lamborghini | 8,983,807 |

3 | Hyundai | Hyundai, Kia, Genesis | 7,244,408 |

4 | Stellantis | Fiat, Peugeot, Jeep, Citroen, Dodge, Ram, Alfa Romeo | 5,510,368 |

5 | BYD | BYD, Fang Cheng Bao | 4,602,436 |

6 | General Motors | Chevrolet, GMC, Cadillac, Buick | 4,547,918 |

7 | Ford | Ford, Lincoln | 4,395,000 |

8 | Geely | Geely, Volvo, Lotus, Polestar, Lynk & Co, Proton | 4,167,717 |

9 | Honda | Honda, Acura | 3,460,000 |

10 | Suzuki | Suzuki | 3,295,013 |

1. Toyota

With 11,322,575 vehicles sold in 2025, Toyota Group remains in a league of its own. Its 12.2% share of the global market is not just a statistic, it's a statement. The Japanese conglomerate, which includes Lexus, Daihatsu, and Hino, sold more vehicles than General Motors, Ford, and Geely combined. The Toyota RAV4 continued to be the world's best-selling individual model, edging out the Tesla Model Y, a fact that speaks volumes about where mainstream consumer demand actually sits.

Toyota's resilience comes from a deliberate refusal to bet exclusively on any single powertrain. While competitors rushed headlong into full electrification, Toyota doubled down on hybrids, maintained ICE production for markets that need it, and grew volume 6% year-over-year in the first half of 2025 alone. Critics called the strategy cautious. The sales figures say otherwise.

2. Volkswagen

Volkswagen Group, with 8,983,807 units sold under its vast umbrella of brands, VW, Audi, Skoda, SEAT, Porsche, Lamborghini, Bentley, and more, holds second place comfortably on paper. But the German giant lost nearly a full percentage point of global market share, and its Asian volumes dropped 6.6%. Europe remains its fortress, where it grew 4.5%, but Europe alone won't be enough if Chinese automakers continue flooding global markets with competitive, affordable EVs.

Oliver Blume, Volkswagen's CEO, has been on a diplomatic offensive, calling China not just a sales market but "a source of innovation" and "a key pillar of the global value system." That framing tells you everything, VW is no longer dictating terms to the Chinese market. It's negotiating.

3. Hyundai-Kia

Third place belongs to Hyundai Motor Group, Hyundai, Kia, and Genesis, with 7,244,408 units. The Korean conglomerate grew its global share to 8%, posting strong gains in America (+5.7%), though it slipped in Europe (-1.7%). Hyundai-Kia may not dominate headlines the way Toyota or Volkswagen do, but it has quietly become one of the most well-rounded automotive groups on earth, competitive across ICE, hybrid, and EV segments simultaneously.

4. Stellantis

Stellantis, the sprawling 14-brand alliance born from the Fiat-Chrysler and PSA merger, settled into fourth place with 5,510,368 vehicles, a result that sounds respectable until you remember the turbulence the company has been through.

CEO Carlos Tavares departed in late 2024 amid boardroom conflict, and the company spent much of 2025 in a period of strategic reset. Still, a 31.9% surge in Asian sales suggests the restructuring is beginning to find direction. Whether it lasts is another question entirely.

5. BYD

Here's the storyline that deserves the most attention: BYD, at fifth place with 4,602,436 vehicles sold, has now surpassed Tesla to become the world's number one seller of pure electric vehicles. Pure EV sales at BYD rose 27.86% year-over-year, reaching 2.26 million battery-electric units alone. Its overseas sales exploded 145% to over 1.05 million vehicles, a global expansion push that's barely getting started.

BYD's secret weapon is vertical integration. It manufactures its own batteries, controls its own supply chain, and can undercut competitors on price in ways that Western and Japanese automakers structurally cannot. A 31% year-over-year growth rate made BYD the fastest-climbing brand in the global top ten. By the end of 2025, it was projected to close in on Ford in total brand sales.

This is no longer a company to watch. It's a company the rest of the industry needs to answer.

6. General Motors

General Motors ranks sixth with 4,547,918 units, holding its position through the combined muscle of Chevrolet, GMC, and Cadillac. In North America, GM remains a force, pickup trucks and large SUVs still print money, and its EV push through the Ultium platform has gained traction domestically. But globally, the picture is more complicated. Asia continues to be a drag, and the gap between GM and the Chinese groups climbing the rankings is narrowing faster than Detroit would like to admit. Being the biggest automaker in America is one thing. Being competitive in a world where BYD ships over a million vehicles overseas annually is an entirely different challenge.

7. Ford

Ford Motor Company settles into seventh with 4,395,000 units, leaning on its core Ford brand with Lincoln serving as a thin premium counterweight. Ford's truck franchise, the F-Series , remains the single best-selling vehicle line in the United States, and that loyalty keeps the volume respectable.

But Ford's global ambitions have repeatedly run into headwinds: its EV division posted significant losses, international market share has stagnated, and the company has been forced into strategic retreats across multiple regions.

The uncomfortable truth Ford must now confront is this: Geely Group, a Chinese conglomerate most Americans couldn't have identified two years ago, is expected to overtake it in total global sales before this year closes.

8. Geely

Geely Holding Group arrives at eighth place with 4,167,717 vehicles, its first time cracking 4 million units annually, on the back of a staggering 67.2% boom in EV sales. Geely's portfolio is broader than most people realize: it includes Volvo, Lotus, Polestar, Proton, and Lynk & Co, alongside its domestic brands. EV sales from the group surged 57.7% in 2025, pushing its share of the global EV market to nearly 10%.

The trajectory is unmistakable. Geely ahead of Ford before year's end is not a prediction, it's a formality.

9. Honda

Honda Motor Group, at ninth with 3,460,000 vehicles, had a difficult year. Asian sales, its heartland, fell 16.8%, contributing to a 6.7% overall volume decline. Honda dropped two positions in global rankings, and the structural pressure from Chinese brands in its home turf of Asia is not easing.

The alliance talks with Nissan collapsed. Honda now navigates its next phase largely alone. For a company that built its global reputation on reliability and efficiency, the current trajectory is a sobering wake-up call.

10. Suzuki

And then there's the real plot twist of 2025: Suzuki, at 3,295,013 vehicles, earns the tenth spot, a first-time entry into this exclusive list. Suzuki's dominance in South and Southeast Asian markets, where affordable small cars are non-negotiable, gave it the volume foundation to squeeze into the global top ten.

It replaced Nissan, which tumbled out of the rankings amid declining volumes, the fallout from the failed Honda merger, and ongoing struggles in China. Don't underestimate Suzuki's staying power, in markets where price is everything and reliability is king, it has no serious challenger.

Conclusion

Three of the world's ten largest automotive groups, BYD, Geely, and arguably Stellantis (with its growing Chinese operations), are now deeply tied to China's industrial machine. BYD, Geely, Changan, SAIC: these names were novelties a decade ago. They are now strategic threats to every legacy automaker with ambitions in Asia, Europe, or emerging markets.

Changan Group is already knocking on Suzuki's door for eleventh place, and if current momentum holds, next year's top ten may look different again.

The question that will define the next five years is not whether Chinese automakers can compete globally. They already are. The real question is how fast legacy manufacturers in Europe, Japan, and America can adapt, and whether adapting will even be enough.

-original.webp)

-original.webp)

-original.webp)